In 2026, digital-currency tax work is less about “what is crypto?” and more about proof, reporting, and reconciliation. Governments are tightening third-party reporting, and tax authorities are getting better data. For accounting and advisory firms—especially those supporting global clients—this is the year to operationalize digital-asset tax controls.

XMC Asia can use 2026 as a positioning moment: help clients stay compliant, avoid overpayment/underpayment, and build audit-ready records across wallets, exchanges, and jurisdictions.

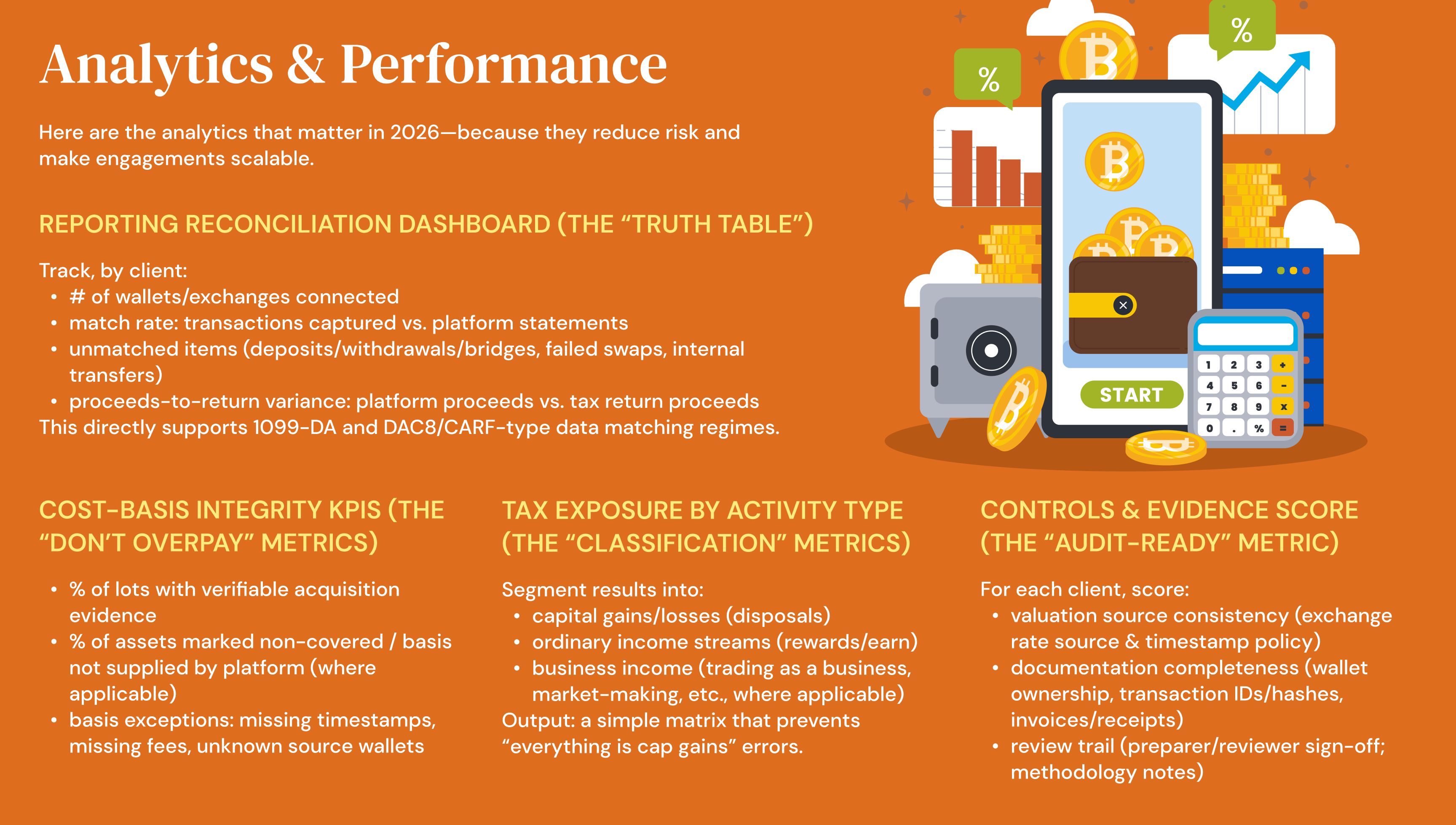

Key Benefits

Stronger compliance as reporting regimes turn on

Three big regimes are shaping 2026:

- EU DAC8: EU rules expand administrative cooperation and tax transparency to crypto-assets, entering into force on 1 January 2026.

- OECD CARF: many jurisdictions aim to collect information during 2026 to enable first exchanges in 2027 (common implementation pattern).

- US Form 1099-DA: IRS digital-asset broker reporting is rolling out, with Form 1099-DA being the standardized reporting mechanism (IRS guidance and form updates are live).

What this means for firms: client tax positions will increasingly be cross-checked against broker/platform data, so the winning play is reconciling early and maintaining defensible records.

Lower risk of “tax overpayment” caused by incomplete statements

A practical 2026 issue: early 1099-DA reporting can emphasize gross proceeds, while taxpayers still must substantiate cost basis and adjustments. If clients rely on proceeds alone, they can overstate taxable gains.

How XMC Asia helps: implement a repeatable process for basis tracing across exchanges/wallets, and document methodologies (FIFO/Specific ID where permitted, etc.) in a workpaper-ready format.

Clearer treatment of taxable events (beyond “selling crypto”)

Firms should ensure clients understand that tax events often include:

- selling crypto for fiat

- trading one token for another

- using crypto to pay for goods/services

- earning crypto (staking, rewards, mining, airdrops—often treated as income depending on local rules)

The core risk is misclassification + missing supporting documentation (timestamps, valuations, fees, wallet ownership).

Global expansion support: aligning tax + regulatory requirements

Digital-asset businesses and even “non-crypto” companies holding digital assets face growing regulatory overlays. For example, in the Philippines, regulators have issued/expanded frameworks around crypto-asset service providers (CASPs) and VASPs.

Firms add value by coordinating: tax compliance + reporting readiness + operational controls (KYC, record retention, governance).

Conclusion

In 2026, digital-currency taxation is becoming an evidence discipline. Reporting regimes (DAC8, CARF, 1099-DA) are expanding the amount of third-party data available to tax authorities, and clients who don’t reconcile and document properly risk penalties, audits—or simply paying the wrong amount of tax.

XMC Asia can lead with a practical promise: clean records, reconciled reporting, defensible tax positions—and deliver it through standardized workflows, analytics, and governance that scale across jurisdictions.

References

- European Commission — DAC8 (Directive on Administrative Cooperation): crypto-asset reporting rules enter into force 1 January 2026

- OECD — CARF Monitoring and Implementation Update (Nov 2025)

- OECD — Jurisdictions committed to implement CARF (Last update: 19 Feb 2026)

- IRS — Final regulations and related guidance for broker reporting on digital assets (Form 1099-DA rollout)

- IRS — About Form 1099-DA