AI is already reshaping audit—especially in planning, risk assessment, and high-volume testing—but it’s not “taking over” the profession. The future looks more like AI-augmented assurance: machines accelerate coverage and pattern detection, while auditors remain accountable for judgment, skepticism, and conclusions.

Firms like XMC Asia can turn this shift into an advantage by deploying AI responsibly—improving audit quality, expanding testing coverage, and strengthening documentation—without compromising professional standards.

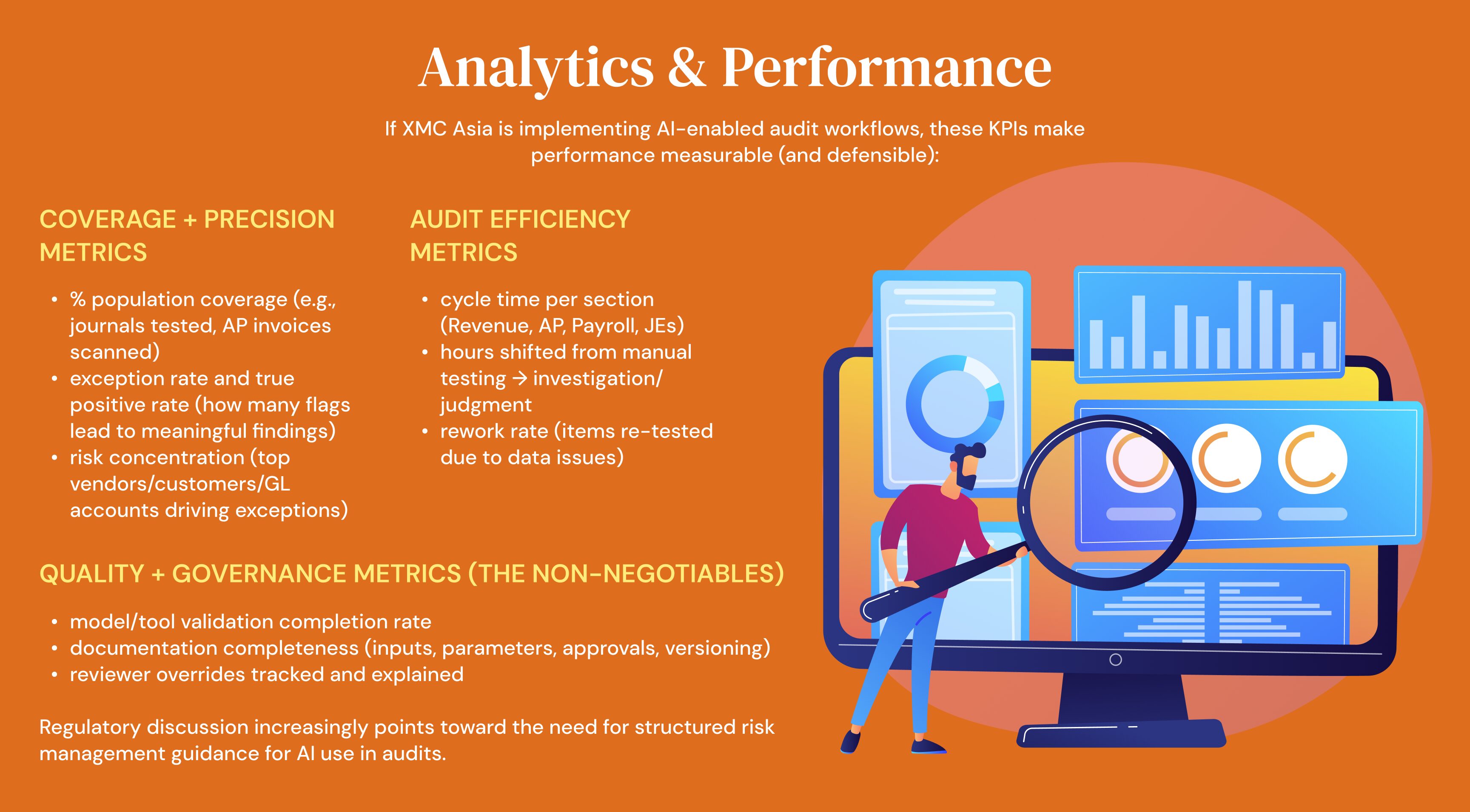

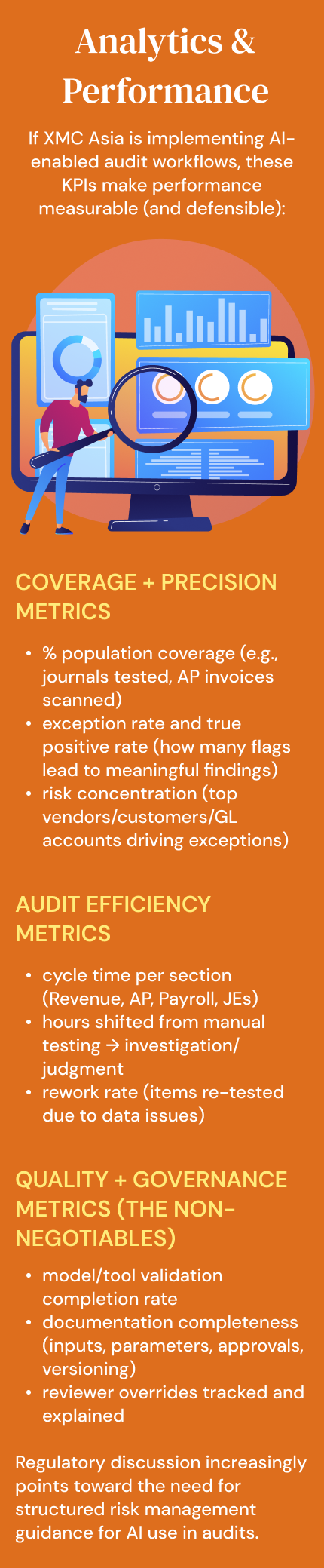

Key Benefits

Higher coverage, faster: from sampling to broader testing

One of AI’s strongest contributions is scale. AI-enabled tools can help teams analyze large populations (e.g., journals, transactions) and triage risk items for deeper follow-up—moving audits beyond purely manual sampling in many areas.

What it replaces (often):

- manual data scrubbing and matching

- repetitive reconciliations and tie-outs

- basic exception identification

What it does not replace:

- deciding whether exceptions are evidence of misstatement, fraud, or process breakdown

- determining sufficiency/appropriateness of audit evidence

- the auditor’s final evaluation and opinion

Better risk assessment through anomaly detection and smarter analytics

AI can flag unusual patterns (timing, counterparties, round-dollar behavior, out-of-hours postings) and support a more targeted audit approach. Regulators and standard-setters are actively engaging how technology-based tools affect audit procedures and quality.

Stronger documentation and repeatability—when governed properly

AI workflows can improve consistency by standardizing:

- data pipelines and testing steps

- evidence packaging and linking to assertions

- variance explanations and audit trail structure

But this only holds if firms implement risk management and governance around AI use—something regulators are explicitly emphasizing.

A new assurance frontier: auditing AI itself

As companies deploy AI in finance operations (credit decisions, forecasting, fraud monitoring, approvals), auditors increasingly need to evaluate AI-driven processes and controls—not just traditional systems.

This creates a practical service opportunity for XMC Asia: helping clients strengthen AI governance, control design, and documentation so audits remain smooth and defensible.

What AI Can Replace (or Mostly Automate)

✅ High-volume, rules-based work

- extracting and normalizing data from multiple systems

- matching, deduplication, and basic reconciliations

- full-population scans for anomalies (journals, AP, AR, payroll)

- drafting routine workpapers and summaries (with human review)

✅ Audit support tasks that are pattern-heavy

- trend analysis and variance drivers

- outlier detection (Benford-like patterns, round-dollar clustering)

- document classification and indexing for evidence retrieval

Important caveat: AI output is only as reliable as the data quality, model controls, and validation around it—overreliance is a known risk theme in research and practice.

What AI Cannot Replace (and Why It Matters)

❌ Professional judgment and skepticism

AI can suggest “risk,” but it cannot own skepticism. Auditors must still:

- challenge management assumptions

- decide what evidence is sufficient

- assess whether inconsistencies point to error, bias, or fraud

- determine the implications for the audit opinion

❌ Accountability and ethical responsibility

Audit is ultimately a public-trust function. Standards, legal accountability, and professional ethics place responsibility on the auditor—not the tool.

❌ Contextual understanding of the business

AI struggles with nuance that auditors rely on:

- “Does this explanation make sense for this business model?”

- “Is this control truly operating, or just documented?”

- “Is the risk new, emerging, or strategically masked?”

❌ Assessing reliability of evidence and tools

Even when AI helps gather evidence, auditors must evaluate:

- whether underlying data is complete/accurate

- whether the AI tool behaves as intended

- whether results are explainable enough to support conclusions

Standard-setters are actively working through how existing auditing requirements map to technology-enabled procedures.

Conclusion

AI will replace some audit tasks, but it won’t replace the auditor. The future of audit is a hybrid model where AI expands coverage and speed—while humans remain responsible for skepticism, judgment, ethics, and the final opinion.

For firms like XMC Asia, the winning approach is clear: adopt AI where it improves audit quality and efficiency, but pair it with strong governance, tool validation, and reviewer discipline. The result is an audit that is faster and more credible—exactly what stakeholders will demand as AI becomes embedded in every business process.

References

- PCAOB — AI and the Pursuit of Audit Quality: A Regulatory Perspective (Sep 16, 2025)

- PCAOB — Data and Technology (standard-setting & research)

- PCAOB — Release No. 2024-007 (technology-assisted analysis amendments) (PDF)

- IAASB — Technology Position announcement (Oct 3, 2024)

- IAASB — Technology Quality Management Roundtables: Outcomes & Next Steps (Feb 10, 2026)